{kind=link}

By Stacey Pogue and Abigail Knapp

It’s the start of rate review season for state insurance departments. Although most proposed premium rates for 2027 Marketplace coverage are not due to federal regulators until mid-July and will not be public until the end of July, some state regulators require insurers to submit proposed rate filings in May or June and release varying levels of information early in the process. These early rate filings provide an initial look at how insurers are responding to market trends, such as rising health care costs, as well as policy changes that affect Marketplace premiums.

Last year, a trio of federal policy changes—expiration of enhanced premium tax credits, enactment of H.R. 1 (also called the “One Big Beautiful Bill”), and adoption of the federal “Marketplace integrity” rule—caused unprecedented net (after federal subsidies) premium increases and contributed to the largest proposed average gross premium increases in nearly a decade.

As insurers develop their 2027 rates this spring, they must contend with federal policy changes that are causing upheaval in the individual market. The individual market is projected to shrink by 17% – 26% this year, with ongoing implications for 2027 rates.

Insurers must also contend with uncertainty stemming from the annual federal Marketplace rule update, known as the Notice of Benefit and Payment Parameters (NBPP). This year, the Centers for Medicaid and Medicare Services (CMS) not only adopted large-scale changes in the NBPP, but did so later in the year than usual, after rates were due in some states.

The following is a roundup of information from proposed 2027 Marketplace rate filings made publicly available to date, which provide some early clues about the trajectory of and reasons behind 2027 Marketplace rate increases.

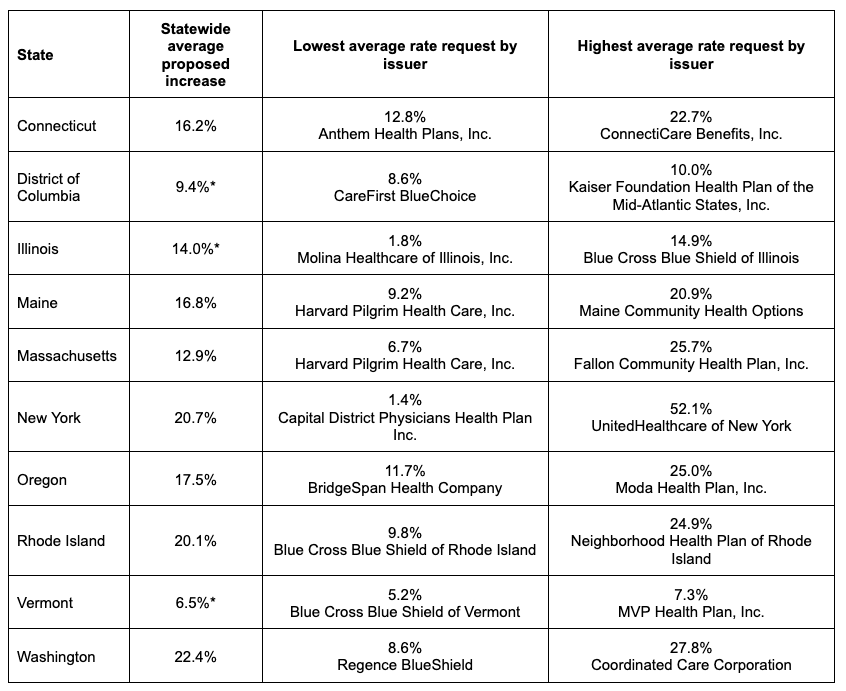

Double-digit proposed rate increases continue in 2027

Early rate filings for 2027 Marketplace plans signal rate increases for next year, often substantial ones. Statewide average proposed 2027 increases released thus far range from 6.5% in Vermont to 22.4% in Washington.

These statewide averages are generally comparable to the significant proposed rate increases seen in states’ early filings last year. Last year’s nationwide median proposed increase of 18% was the highest in nearly a decade, and nearly triple the median proposed increases from the two prior years (6% in 2024 and 7% in 2025).

2027 Proposed Marketplace Rate Increases

Note: Data reflect 2027 ACA individual market (or Massachusetts merged market) rate filings that include Marketplace plans made publicly available as of June 15, 2026. Statewide average proposed rate change as calculated by the state, where available. Those marked with an asterisk (*) are a weighted average using enrollment information from 2027 rate filings. See linked source materials for further information. Connecticut, District of Columbia, Illinois, Maine, Massachusetts, New York, Oregon, Rhode Island, Vermont, and Washington.

With an average requested increase of 22.4 percent, insurers in Washington are seeking the most significant statewide rate hike to date. “I know the requested rate changes will be difficult for individuals and families,” said Insurance Commissioner Patty Kuderer. “We’re going to spend the next several months reviewing every assumption made by the insurers to make sure their requests are justified.” Enrollment through the Washington Health Benefit Exchange has declined 13% since 2025, a trend primarily attributed to the expiration of enhanced premium tax credits (ePTC).

Oregon regulators also acknowledged the impact of ePTC expiration on declining enrollment and proposed rate increases. “Oregon consumers are facing challenging times with expiring premium tax credits, rising health insurance rates across the country, and two carriers leaving the Oregon market,” said TK Keen, Oregon’s Insurance Commissioner.

High costs and market uncertainties lead to carrier exits

At least six insurers have announced that they will exit ACA Marketplaces in plan year 2027: Cigna Health, CareSource, PacificSource, Baylor Scott and White, Providence Health, and Mending (formerly Taro Health). As a result, roughly 650,000 people across a third of states will need to select new plans next year.

Insurers cited rising costs, declining enrollment, and policy uncertainty as factors behind their decisions. Cigna president and incoming chief executive Brian Evanko indicated that there was no “clear path” to scale the company’s ACA business, which has been shrinking in recent years; enrollment in Cigna Marketplace plans dropped 17% compared to the first quarter of 2025. A spokesperson for PacificSource indicated that rising health care costs have become unsustainable, while Baylor Scott & White pointed to individual marketplace “complexities.” Providence CEO Erik Wexler noted that changes in state and federal regulation have made it increasingly difficult for regional, not-for-profit health plans like Providence to thrive. “Meanwhile, the larger insurance companies have consolidated significantly, giving them the size and resources to operate more efficiently. This has left us in an untenable situation,” said Wexler.

As insurers exit the ACA Marketplaces, consumers are left with fewer choices for coverage. With the exits of Providence and PacificSource, only four insurers will offer Marketplace plans in Oregon. However, Oregon’s insurance commissioner noted that consumers in every county will have at least three options to choose from. Exits also create uncertainty for insurers that remain in the market, as they have little insight into the risk profile of consumers newly enrolling in their plans.

Insurers point to federal policies and higher medical costs as driving rate increases

A handful of states publish the detailed supporting documentation filed by insurers relatively early compared to other states. These documents explain the assumptions used by insurers and their justifications for proposed rate changes. We reviewed 40 insurer justifications from eight of these states, Connecticut, the District of Columbia, Illinois, Maine, Massachusetts, Oregon, Vermont, and Washington, to better understand the primary drivers of 2027 Marketplace rate increases.*

As was true last year, insurers in our sample of 2027 rate filings frequently cited rising health care costs and impacts from the expiration of ePTCs as key drivers of proposed rate increases.

Expiration of enhanced premium tax credits pushes some rates higher for the second year

Between 2021 and 2025, Congressional action enhanced the generosity of the ACA’s premium tax credits. These ePTCs made Marketplace coverage much more affordable, leading to record Marketplace enrollment—24 million people—in 2025. Congress failed to extend ePTCs, and they expired at the end of 2025.

Most insurers pointed to the end of ePTCs as a key contributor to large 2026 rate increases, driving rates 4% to 6% higher on average than they otherwise would have been. In 2026 rate filings, insurers anticipated that healthier people would be more likely to drop coverage as net premiums rise. Remaining enrollees would be sicker on average—referred to as increased “morbidity” by insurers—increasing average claims costs and driving up rates.

Early rate filings signal that rate impacts from the end of ePTCs will continue into 2027. Insurers in our sample frequently pointed to the expiration of ePTCs as a key factor behind 2027 proposed rate increases, with many pointing to a smaller, sicker risk pool. Mass General Brigham Health Plan in Massachusetts explains that the end of ePTCs reduced “the financial support that previously made health insurance more accessible,” leading to “the loss of lower-risk members.” Community Health Plan of Washington noted declining enrollment in 2026 and “anticipate[s] further market size reduction in 2027.” It expects “the remaining risk pool in 2027 to have higher healthcare needs, on average.”

Insurers also pointed to emerging trends they are monitoring to assess the impacts of ePTC expiration. MVP Health Plan in Vermont believes it has not seen the “full impact” of expired ePTCs yet, as it “continue[s] to see retroactive coverage terminations for non-payment of premium.” Blue Cross Blue Shield of Vermont said the “large” adjustment it made to reflect higher morbidity was informed by its analysis of prior claims costs of people who had dropped coverage as of February 2026. In addition to reduced enrollment, Moda Health Plan in Oregon has observed “a shift in emerging 2026 utilization trends,” related to ePTC expiration.

Some filings quantified the impacts related to expired ePTCs on 2027 rates. Fallon Community Health Plan in Massachusetts noted that 3.3 percentage points of its 25.7% proposed increase is due to morbidity impacts from policy changes, including expired ePTCs. ConnectiCare Benefits in Connecticut attributes a 5% premium increase to the scheduled expiration of ePTC-related state subsidies at the end of 2026. (Connecticut implemented a temporary state-funded subsidy to backfill a portion of expired ePTCs in 2026, and the state directed insurers to assume it expires as scheduled at the end of this year.) MVP Health Plan of Vermont said the adjustment it made for increased morbidity from the expiration of ePTCs translates to an additional $48 per member per month in claims costs.

2027 NBPP adds a layer of uncertainty

The recently adopted 2027 NBPP includes broad changes that CMS projects will reduce enrollment by 1.2 to 2 million people next year, including additional paperwork burdens at enrollment, increases in plans’ out-of-pocket costs, and erosion of ACA consumer protections. Changes in the rule will have implications that insurers need to consider as they set 2027 premiums. For example, in comments on the proposed rule, insurers and state regulators raised concerns that some provisions could cause healthier individuals to leave the risk pool, leading to higher premiums.

The later-than-usual timing of the rule creates challenges for insurers and regulators during the rate review process. CMS published the proposed rule on February 11, 2026, as insurers were developing 2027 plans and rates, and adopted it on May 20, 2026, after plans and rates were due in some states. Adding to uncertainty, a coalition of cities, physicians, and small businesses filed a lawsuit on June 3, 2026, challenging many of the rule’s provisions. A similar lawsuit from last year resulted in a stay of many provisions, including some similar to those adopted in the 2027 NBPP. State and federal regulators may allow insurers to refile their rates to account for changing policies through August 12, 2026.

A few filings in our sample discussed impacts–whether projected or unknown–from the 2027 NBPP. A few filings reference uncertainty about the ultimate impacts. Blue Cross Blue Shield of Vermont, for example, noted uncertainty because, when it submitted its proposed rates, the NBPP “ha[d] not been finalized yet.” Coordinated Care Corporation of Washington indicates it “will seek regulatory approval to file revised rates” if “material rating impacts” arise, including from risk adjustment updates in the 2027 NBPP.

Both insurers in Vermont noted impacts from expanding catastrophic plan eligibility (beyond primarily people under age 30), as codified in the 2027 NBPP. MVP Health Plan of Vermont proposed a 109% premium increase for its catastrophic plan. It alluded to historically lower rates for its catastrophic plan when such plans were limited primarily to people under age 30, but anticipates that broader eligibility will shift the risk profile of catastrophic plan enrollees to be similar to that of metal-level ACA plans.

A few insurers alluded to challenges using the specific method for calculating cost sharing reduction payments required by the rule. For example, Community Health Options in Maine acknowledged the method spelled out in the regulation, but noted that it “received approval from the Maine [Bureau of Insurance] to use an estimation approach” instead.

Rising cost trends contribute to rate increases

Increasing health care costs are a key driver of health insurance rate changes in 2027, as they are in most years. Rate filings include insurers’ assumptions about the year-over-year change in health care costs, referred to as medical cost trend (or “trend”). Components of trend include anticipated changes to unit prices (the amount insurers pay providers for health care goods and services) as well as utilization (the frequency or volume of services delivered). PwC projects that trend will be high in 2027, reaching 8.5% in the individual market.

In early filings, insurers frequently attribute requested rate increases to higher provider reimbursements, greater utilization, and general medical cost inflation. UnitedHealthcare of Illinois noted that key health care cost trends include annual increases in reimbursement rates to health care providers. United also indicated that the number of office visits and other services continues to grow and that shifts in the intensity of care and in the use of different types of health care services affect its costs. Additionally, many insurers specifically cite rising pharmaceutical spending, particularly for high-cost specialty drugs. Beyond pharmacy costs, a few insurers mentioned other specific services impacting cost trends, including hospital stays, outpatient surgeries, and mental health/behavioral health visits.

A couple of insurers noted that increased provider consolidation has contributed to rising costs. Premera Blue Cross in Washington indicated that, “high unit cost increases reflect continued pressure from provider contract negotiations, including provider requests for double-digit reimbursement increases in certain markets.” It further noted that limited competition and regional monopolies have reduced downward pricing pressure.” Relatedly, Anthem Health Plans in Connecticut argued that the state’s health care cost growth benchmark fails to fully account for factors driving up health care costs, including but not limited to “high cost specialty drugs and treatments, increases in healthcare labor costs due to clinical workforce shortages, and provider consolidation.”

Some insurers provide detailed estimates that break down their trend assumption into components, including health care prices and utilization. When included in rate filings, the impact of provider reimbursements versus utilization on overall cost trend varies across states and insurers. For instance, insurers in Oregon generally indicated that prices had a greater impact on projected trend than utilization, while factors underlying trend projections in Massachusetts were more mixed. For example, BridgeSpan Health Company in Oregon and Wellsense Health Plan in Massachusetts both projected trend near 10% for 2027. However, BridgeSpan projected that prices will have the greatest impact on trend in 2027, while Wellsense projected that prices and utilization/mix of services delivered will have a relatively equal impact.

Conclusion

The bulk of 2027 Marketplace rate filings are not yet available, but filings from early states foreshadow another bumpy year for ACA Marketplaces. Insurers are facing high health care cost growth, significant drops in enrollment, a worsening risk pool, and an unstable policy environment. Some ACA Marketplace consumers will be affected by insurer exits, and those who do not qualify for financial help may face double-digit rate hikes. A more complete picture of rates and insurer participation in the 2027 Marketplace will emerge as rate filing season progresses.

*Authors’ note: Our review of publicly available, early 2027 individual market rate filings was largely limited to the narratives in the actuarial memoranda that must accompany each rate filing. These memos explain, in lay language, insurers’ past experience, current assumptions, and predictions for the next plan year. The findings summarized in this blog are not necessarily generalizable to the broader universe of individual market rate filings for plan year 2027, nor do they reflect all of the factors underlying rate requests or differences between insurers’ filings in this set of states. The authors thank Max Quan and Logan DeLeire for their assistance with rate filing research and review of the data.